matlab优化工具04二次规划之quadprog

二次规划问题是目标函数为 \(\textbf{x}\) 的二次形式, 约束条件为线性等式或不等式约束

二次规划的一般模型

\[ \begin{aligned} \min \quad & f^T x + \frac{1}{2}x^T \textbf{H} x \\ \text {s.t.} \quad & \textbf{A} \cdot x \leq b \\ & \textbf{Aeq} \cdot x=beq \\ & l b \leq x \leq ub \end{aligned} \]

其中: \(x, b, beq\)是向量, \(f^T\) 为一次项的系数, \(\textbf{A}\)是矩阵,\(\textbf{H}\)是矩阵, \(\textbf{H}\)是矩阵,即二次项系数,用以描述\(x_i^2\) 以及 \(x_i x_j\)项. \(\textbf{A}\)线性不等式,\(\textbf{Aeq}\)线性等式,

当然,二次规划的目标函数中的二次项还可以用元素的形式表达,即 \[ \begin{aligned} \frac{1}{2}\left(h_{11} x_{1}^{2}+h_{12} x_{1} x_{2}+\cdots+h_{1 n} x_{1} x_{n}+h_{21} x_{1} x_{2}+h_{22} x_{2}^{2}+\cdots+h_{n n} x_{n}^{2}\right) \end{aligned} \]

定理: 如果\(\textbf{H}\) 矩阵为正定矩阵, 则二次规划问题是凸问题. 即它的求解与初始值无关,只要有可行解,则一定是全局最优解.

如果二次规划问题非凸,则该函数不能得出原始问题的全局最优解,甚至可能不能得出可行解.

matlab 函数— — quadprog

%% 语法

x = quadprog(H,f,A,b,Aeq,beq,lb,ub)

x = quadprog(H,f,A,b,Aeq,beq,lb,ub,x0)

x = quadprog(H,f,A,b,Aeq,beq,lb,ub,x0,options)

x = quadprog(problem)

[x,fval,exitflag,output,lambda] = quadprog(___)

%% 不解释了, 看前面的fmincon函数

x0 初始值例1

\[ \begin{aligned} min & \quad \left(x_{1}-1\right)^{2}+\left(x_{2}-2\right)^{2}+\left(x_{3}-3\right)^{2}+\left(x_{4}-4\right)^{2} \\ & \text{s.t.} \begin{cases} x_{1}+x_{2}+x_{3}+x_{4} \leqslant 5 \\ 3 x_{1}+3 x_{2}+2 x_{3}+x_{4} \leqslant 10 \\ x_{1}, x_{2}, x_{3}, x_{4} \geqslant 0 \end{cases} \end{aligned} \]

方法一: 根据上述方程,写出标准形式的二次规划

\[ f(x)=x_{1}^{2}+x_{2}^{2}+x_{3}^{2}+x_{4}^{2}-2 x_{1}-4 x_{2}-6 x_{3}-8 x_{4}+30 \]

然后写出 \(\textbf{H}\)和\(f^T\),代码如下:

clc,clear all;format compact;

f = [-2;-4;-6;-8];

H = diag([2,2,2,2]);

A = [1,1,1,1;

3,3,2,1];

b = [5;10];

lb = [0,0,0,0];

ub = [];

x0=[];

options = optimoptions('quadprog','Display','iter');

[x,fval,exitflag,output,lambda] = quadprog(H,f,A,b,[],[],lb,ub,x0,options)

% ---------------------------- 结果 -------------------------

x =

0.0000

0.6667

1.6667

2.6667

fval =

-23.6667方法2 : 采用问题描述的形式 — 结构体

这种模式,不需要手工推导\(\textbf{H}\) 矩阵

%% 问题描述形式 --- 以结构体方式创建

%%

% optimproblem('ObjectiveSense','max') % 最优化问题的创建, ObjectiveSense属性求最大值(默认最小值)

%% optimvar 决策变量的定义,n,m,k 设置决策变量的维度,不设置k则变量维度为n*m

% x = optimvar('x',n,m,k,'LowerBound',lb,'UpperBound',ub)

clc,clear all;format compact;

x = optimvar('x',4,1,'LowerBound',[0;0;0;0],'UpperBound',[]);

objec = sum( (x - [1;2;3;4]).^2 );

prob = optimproblem('Objective',objec);

prob.Constraints.cons1 = sum(x) <= 5;

prob.Constraints.cons2 = 3*x(1) + 3*x(2) + 2*x(3) + x(4) <=10;

sols = solve(prob);

x=sols.x

%% ---------------------------- 结果 -------------------------

x =

0.0000

0.6667

1.6667

2.6667

%% 上述问题还可以简化,利用向量的形式给出

clc,clear all;format compact;

x = optimvar('x',4,1,'LowerBound',[0;0;0;0],'UpperBound',[]);

objec = sum( (x - [1:4]').^2 );

prob = optimproblem('Objective',objec);

prob.Constraints.cons1 = sum(x) <= 5;

prob.Constraints.cons2 = [3,3,2,1] * x <=10;

sols = solve(prob);

x=sols.x

%% ---------------------------- 结果 -------------------------

x =

0.0000

0.6667

1.6667

2.6667例2:

\[ \begin{aligned} \min \quad & -2 x_{1}+3 x_{2}-4 x_{3}+4 x_{1}^{2}+2 x_{2}^{2}+7 x_{3}^{2}-2 x_{1} x_{2}-2 x_{1} x_{3}+3 x_{2} x_{3} \\ & \text{s.t. }\begin{cases} 2 x_{1}+x_{2}+3 x_{3} \geq 8 \\ x_{1}+2 x_{2}+x_{3} \leq 7 \\ -3 x_{1}+2 x_{2} \leq-5 \\ x_{1}, x_{2}, x_{3} \geq 0 \end{cases} \end{aligned} \]

由于上述问题采用手工的方法比较麻烦,因此可以采用问题描述的形式求解该问题

clc,clear all;format compact;

x = optimvar('x',3,1,'LowerBound',[0;0;0],'UpperBound',[]);

objec = -2*x(1) + 3*x(2) - 4*x(3) + 4*x(1)^2 + 2*x(2)^2 + 7*x(3)^2 -2*x(1)*x(2) -2*x(1)*x(2) + 3*x(2)*x(3);

prob = optimproblem('Objective',objec);

prob.Constraints.cons1 = [2,1,3] * x >= 8;

prob.Constraints.cons2 = [1,2,1] * x <=7;

prob.Constraints.cons3 = [-3,2,0] * x <= -5;

sols = solve(prob);

x=sols.x

%% ---------------------------- 结果 -------------------------

Solving problem using quadprog.

Your Hessian is not symmetric. Resetting H=(H+H')/2.

Minimum found that satisfies the constraints.

Optimization completed because the objective function is non-decreasing in

feasible directions, to within the value of the optimality tolerance,

and constraints are satisfied to within the value of the constraint tolerance.

<stopping criteria details>

x =

2.2500

0.8750

0.8750上述可以看到 Your Hessian is not symmetric. Resetting H=(H+H')/2. 说明给出了警告,指出自动生成的Hesse 矩阵是非对称的, 所以建议设置H=(H+H')/2 将其转化为对称矩阵. 由于问题描述模式没有输入H矩阵. 因此,应该将问题描述模式转为结构体模型,再来处理H矩阵(这样做不会产生警告,不过最后的结果都是一样的).

>> p = prob2struct(prob);

p =

包含以下字段的 struct:

intcon: []

lb: [3×1 double]

ub: [3×1 double]

x0: []

Aineq: [3×3 double]

bineq: [3×1 double]

Aeq: []

beq: []

f0: 0

solver: 'quadprog'

H: [3×3 double]

f: [3×1 double]

options: []

>> p.H = (p.H + p.H') / 2;

>> x1 = quadprog(p)

x1 =

2.2500

0.8750

0.8750双下标二次规划

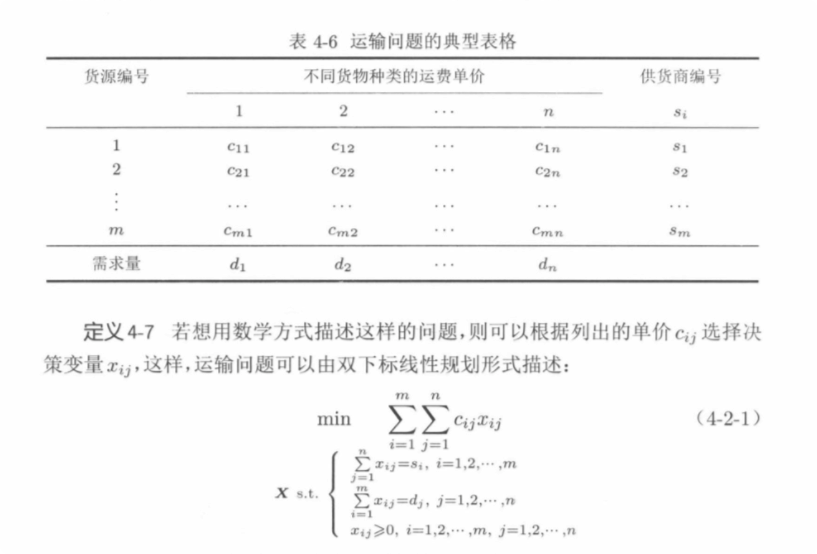

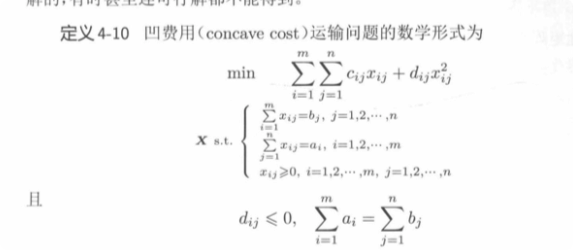

主要是根据线性模型中的运输问题直接扩展而来的, 即把线性模型中的运输问题的目标函数用二次项表示,其他的约束条件都不变

线性模型中的运输问题

双下标二次规划的一个改进版本

%% 对凹费用运输问题的求解,假设 n = 4, m = 6, a,b,C,D 已知;

%% 双虾标的运输问题(凹费用运输问题)

% 已知 n, m,a,b,C,D

clc,clear all;format compact;

n = 4; m = 6;

a = [8,24,20,24,16,12]';

b = [29,41,13,21];

C= [300, 270, 460, 800;

740, 600, 540, 380;

300, 490, 380, 760;

430, 250, 390, 600;

210, 830, 470, 680;

360, 290, 400 ,310];

D = [-7, -4, -6, -8;

-12, -9, -14, -7;

-13, -12, -8, -4;

-7, -9, -16, -8;

-4, -10, -21, -13;

-17,-9,-8,-4];

x = optimvar('x',m,n,'LowerBound',0,'UpperBound',[]);

objec = sum(sum(C .* x + D.* (x.^2)) );

prob = optimproblem('Objective',objec);

prob.Constraints.cons1 = sum(x,1) == b;

prob.Constraints.cons2 = sum(x,2) == a;

sols = solve(prob);

x=sols.x

%% ---------------------------- 结果 -------------------------

Solving problem using quadprog.

The problem is non-convex.

x =

1 1 1 1

1 1 1 1

1 1 1 1

1 1 1 1

1 1 1 1

1 1 1 1

>> 注意: 上述结果不满足约束条件,即得出的结果不是可行解, 这时候, 则需要使用fmincon 函数了

% 由于上述问题采用问题描述方式书写的,这里进行转化,转化为结构体模式

p = prob2struct(prob);

p.solver = 'fmincon'; %转为结构体必须修改必要的参数

f = @(x) sum(C(:) .* x + D(:) .* x.^2);

p.Objective = f; %定义目标函数

ff = optimset;

ff.TolX =eps; % 一个比较苛刻的误差值l

ff.TolFun=eps;

p.options = ff;

p.x0 =100*rand(m*n,1);

x0 =fmincon_global(p,-10,10,n*m,50);

X0 = reshape(x0,m,n)

%% ---------------------------- 结果 -------------------------

X0 =

6.0000 2.0000 0.0000 0.0000

0.0000 3.0000 0.0000 21.0000

20.0000 0.0000 0.0000 0.0000

0.0000 24.0000 0.0000 0.0000

3.0000 0.0000 13.0000 0.0000

0.0000 12.0000 0.0000 0.0000参考:

matlab函数官网

<<薛定宇教授大讲堂卷5 MATLAB最优化计算>>_含目录py.pdf